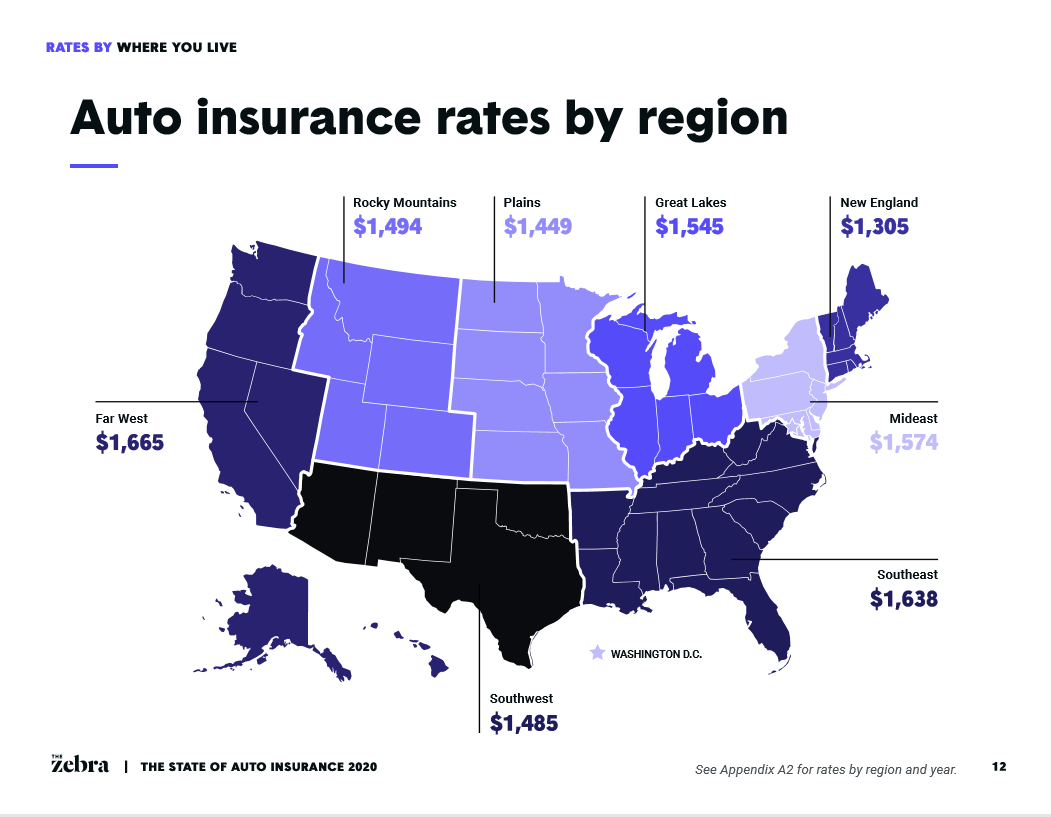

You’ve probably noticed that car insurance rates can vary significantly depending on where you live. The same driver with the same car can pay vastly different premiums in different parts of the country. But have you ever wondered why that is?

It all comes down to a combination of factors that insurers use to calculate risk. You see, insurance companies are always trying to balance their books by matching the premiums they collect with the payouts they make. So, if they think a particular region is riskier, they’ll charge more to account for that risk. Let’s take a deeper dive into the key factors that influence regional car insurance rates.

Weather Patterns: Tornado Alley vs. Sunny California

If you live in the Midwest, also known as Tornado Alley, your car insurance rates might be higher than those in California. That’s because tornadoes and hail storms can cause significant damage to vehicles. Insurers consider the frequency and severity of natural disasters when setting premiums in a particular area. On the other hand, California has a milder climate, with less risk of devastating weather events, which translates to lower insurance rates.

Population Density: Urban vs. Rural

Urban areas tend to have higher car insurance rates due to increased traffic congestion, accidents, and crime rates. Cities like New York or Los Angeles have more drivers on the road, which raises the likelihood of accidents and claims. Rural areas, with fewer cars on the road and less crime, typically have lower insurance rates.

State Laws and Regulations

Each state has its own set of laws and regulations governing car insurance. Some states have minimum coverage requirements, while others have higher thresholds for lawsuits. For example, Michigan has some of the highest car insurance rates in the country due to its no-fault insurance system, which requires insurers to cover medical expenses for drivers injured in accidents. This increases costs for insurers, which are then passed on to consumers.

Local Economic Factors

Economic conditions can also impact car insurance rates. Areas with lower economic growth, higher poverty rates, or higher unemployment may experience more theft or vandalism, leading to higher insurance rates. Conversely, areas with stronger economies and higher incomes tend to have lower insurance rates.

Claims Frequency

Insurance companies also look at claims frequency when determining regional rates. If a particular area has a higher incidence of claims, insurers will adjust their premiums accordingly. For instance, areas with high rates of reckless driving or drunk driving may experience higher insurance rates.

Vehicle Thefts and Vandalism

Some areas are more prone to vehicle thefts and vandalism. Cities with high crime rates or areas with a history of vandalism will likely have higher car insurance rates. This is because insurers assume a higher risk of damage or loss.

Geographic Location

Believe it or not, your geographic location can also influence your car insurance rates. In areas prone to wildfires, earthquakes, or hurricanes, insurance companies may charge more to account for the increased risk of damage or loss.

Now that you know the factors that contribute to regional car insurance rates, you can better understand why your premiums might be higher or lower than someone living elsewhere. Remember, insurance companies are always trying to balance their risk exposure. By understanding these regional factors, you can make more informed decisions about your car insurance coverage and potentially save money in the process.

However, if you’re looking to lower your car insurance rates, regardless of your location, consider shopping around for quotes from multiple insurers. Many companies offer personalized rates that take into account individual factors such as driving history, vehicle make and model, and annual mileage. You may be surprised by the savings you can find by comparing rates and coverage options.