Imagine you’re running a bustling restaurant, and a fire breaks out in the kitchen, forcing you to shut down operations for several months. Or perhaps you’re a retailer whose storefront is damaged in a storm, leaving you unable to serve customers. In either case, the financial impact can be devastating – not just from the physical damage, but from the loss of income and revenue as well.

That’s where business interruption insurance comes in – a vital component of any comprehensive business insurance policy. But what exactly does it cover?

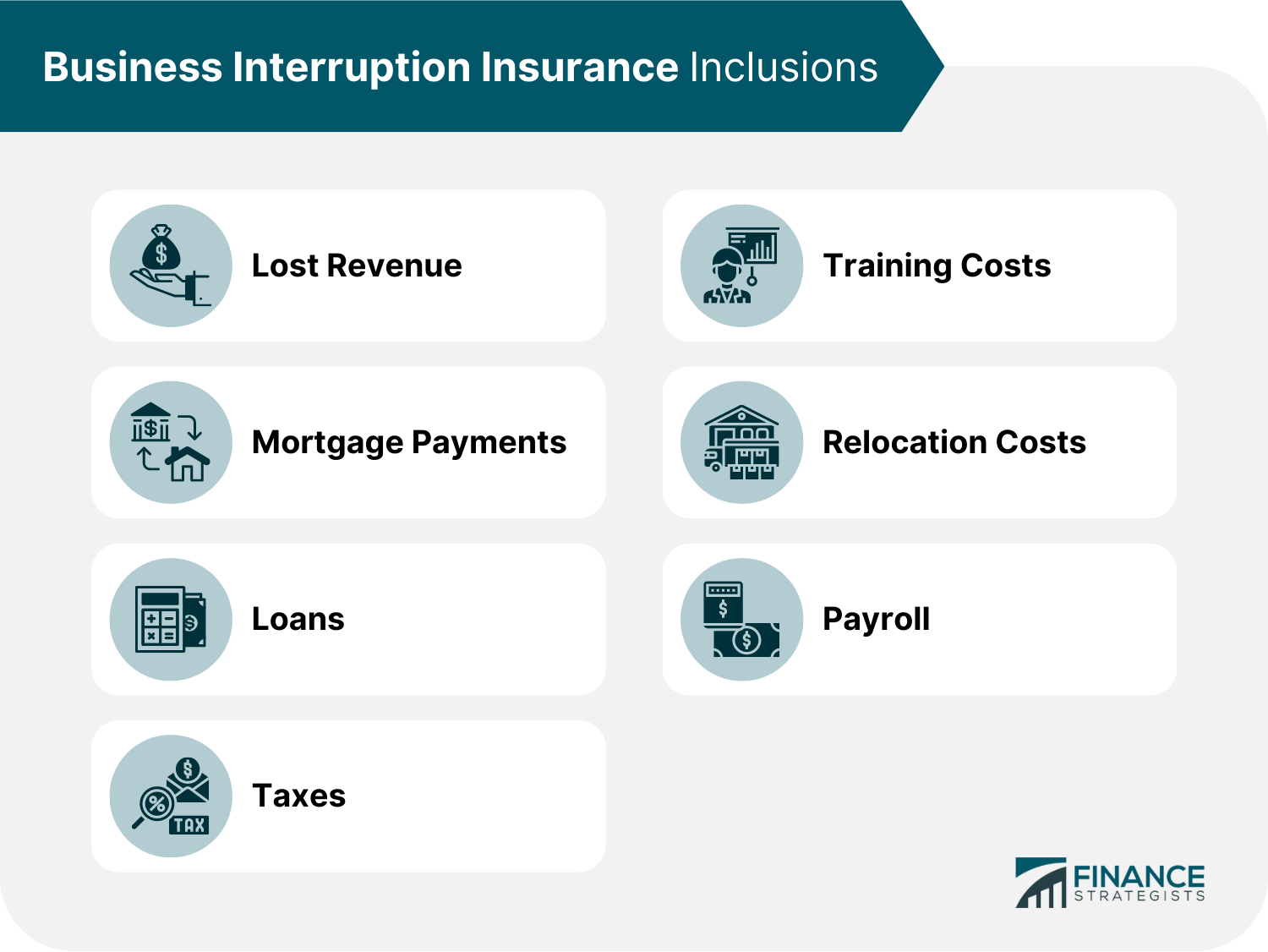

Understanding Business Interruption Insurance

Business interruption insurance, also known as business income insurance, is designed to help businesses recover from a temporary shutdown due to unforeseen events like natural disasters, fires, or equipment failures. This type of insurance provides financial support to cover ongoing expenses, such as employee salaries, rent, and utilities, until your business is up and running again.

What’s Typically Covered

A standard business interruption insurance policy typically covers the following:

- Business Income: This includes revenue lost due to a temporary shutdown, as well as ongoing expenses like payroll, rent, and utilities.

- Extra Expenses: If you need to rent temporary space or equipment to continue operations, this coverage can help offset those costs.

- Ordinary Payroll Expenses: In some cases, business interruption insurance may cover the cost of employee salaries and benefits for a set period, usually up to 90 days.

- Taxes and Fees: This coverage can help with taxes and fees associated with your business, such as sales tax or licensing fees.

- Accounts Receivable: If you’re unable to collect payments from customers due to a shutdown, this coverage can provide financial assistance.

What’s Not Typically Covered

While business interruption insurance provides essential financial support during a shutdown, there are some limitations to be aware of:

- Flooding: Standard policies often exclude flood damage, so you may need to purchase separate flood insurance to protect your business.

- Pandemics: Unfortunately, most business interruption policies do not cover losses related to pandemics or widespread health crises.

- Cyber Attacks: If your business is shut down due to a cyber attack or data breach, you may not be covered unless you have a specific cyber insurance policy.

- Government Actions: If the government forces your business to close due to a public health emergency or other reason, you may not be eligible for business interruption coverage.

How to Choose the Right Policy

When selecting a business interruption insurance policy, consider the following:

- Policy Limits: Make sure the policy limit is sufficient to cover your business’s monthly expenses.

- Deductible: Check the deductible amount and ensure it’s affordable for your business.

- Waiting Period: Understand the waiting period before coverage kicks in – this can range from a few days to several weeks.

- Coverage Period: Determine the length of time coverage will be provided – typically 6-12 months, but sometimes up to 24 months.

By understanding what business interruption insurance covers, you can protect your business from the unexpected and ensure a smoother recovery in the event of a temporary shutdown. Take the time to review your policy options carefully and choose the coverage that best suits your business needs.