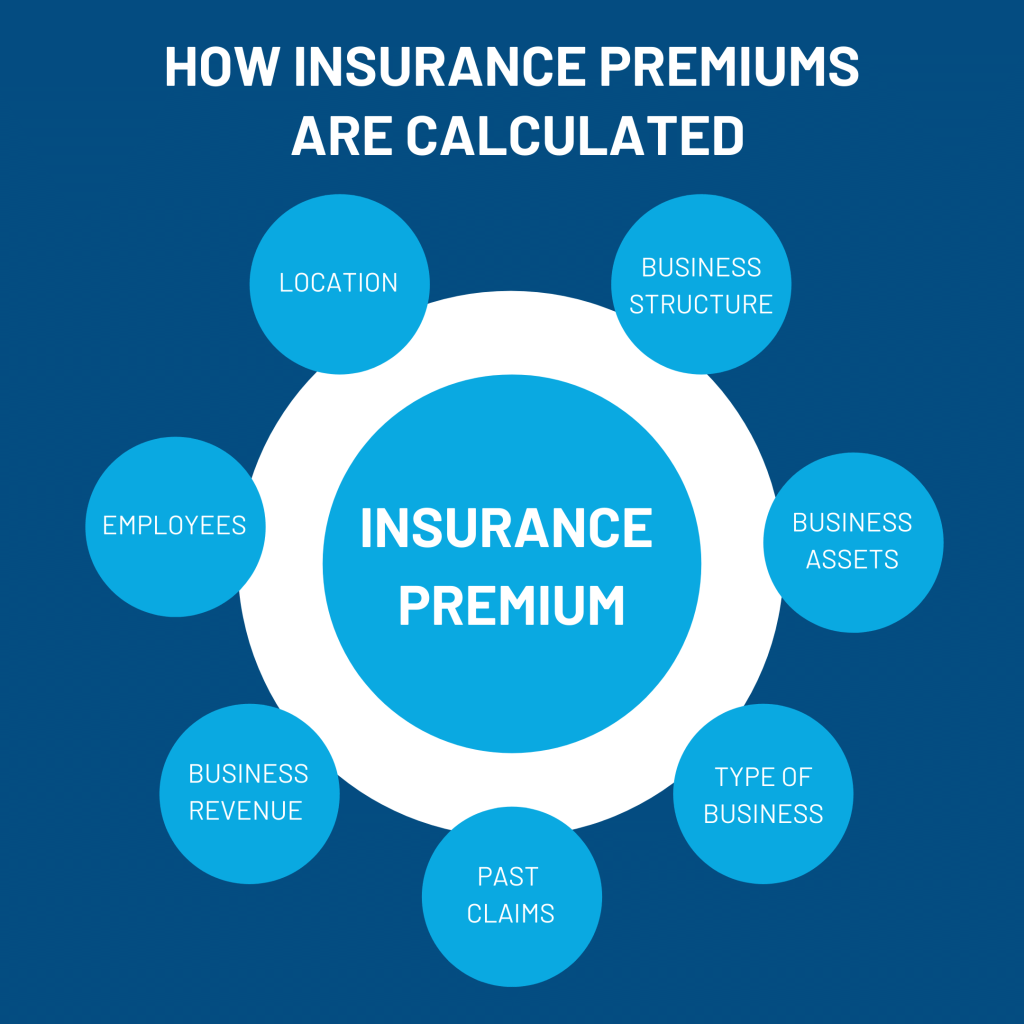

The Lowdown on Insurance Claims: How They Impact Your Premiums

Think of insurance claims like a double-edged sword. On one hand, filing a claim can help you recover from a financial setback or cover unexpected expenses. On the other hand, it can also lead to increased premiums, which can put a dent in your wallet. So, how exactly do insurance claims affect your premiums?

Let’s dive into the world of insurance claims and explore the factors that influence premium increases. By understanding these dynamics, you’ll be better equipped to make informed decisions when dealing with insurance claims.

The Claims Process: A Refresher

Before we dive into the nitty-gritty, let’s quickly review how the claims process works. When you file a claim, your insurer will typically follow these steps:

- Review and assessment: Your insurer will assess the claim to determine if it’s valid and covered under your policy.

- Investigation: The insurer may conduct an investigation to verify the details of the claim.

- Payout or denial: If the claim is approved, your insurer will issue a payout. If not, you’ll receive a denial notice explaining why.

The Impact on Premiums

So, how do insurance claims affect your premiums? The short answer is that it depends on various factors. Here are some key considerations:

- Claim frequency and severity: If you’ve filed multiple claims in a short period, your insurer may view you as a higher risk. Similarly, if you’ve filed claims for significant amounts, your premiums may increase.

- Type of claim: The type of claim you file can also impact your premiums. For example, if you file a claim for a minor issue, it may not significantly affect your premiums. However, if you file a claim for a more serious issue, such as a car accident or property damage, your premiums may increase.

- Insurer’s claims experience: Your insurer’s claims experience can also influence premium increases. If your insurer has paid out multiple claims in your area or for similar incidents, they may raise premiums to account for the increased risk.

- State and local regulations: Insurance regulations vary by state and locality. Some states have laws that limit premium increases following claims.

Premium Increase Scenarios

To give you a better idea of how insurance claims can affect your premiums, let’s explore some common scenarios:

- Single claim: If you file a single claim for a minor issue, such as a broken window or a small fender bender, your premiums may not increase significantly. However, if you file a claim for a more serious issue, such as a car accident or property damage, your premiums could increase by 10% to 20%.

- Multiple claims: If you file multiple claims within a short period, your premiums may increase more significantly. For example, if you file two claims within a year, your premiums could increase by 20% to 30%.

- High-cost claim: If you file a claim for a high-cost incident, such as a severe car accident or significant property damage, your premiums could increase substantially, potentially by 30% to 50% or more.

Mitigating Premium Increases

While you can’t avoid filing claims entirely, there are steps you can take to mitigate premium increases:

- Choose a high deductible: By choosing a higher deductible, you may be able to lower your premiums and reduce the likelihood of filing claims.

- Bundle policies: Bundling multiple policies with the same insurer can sometimes lead to discounts.